Taking the Airbus to the IKEA Cloud

This article is part of a series on (European) innovation and capabilities.

The very short version:

- All of computing is moving to the cloud at a rapid pace, including (government) parts you might want to keep under your own control

- Europe has no relevant ‘hyperscaler’ cloud providers at all, and there is a desire to change this by policy means

- Competing with the IKEA-concept is nearly impossible. Offering IKEA-like products but then with a smaller range is not an attractive proposition. You can’t replicate IKEA without a LOT of upfront work

- Replicating a company like Airbus (or ASML) is similarly very hard: both companies (and their ecosystems) are one of the very few places where you can buy modern wide body jets and extreme UV wafer steppers. Their products are technically incredibly advanced.

- The ‘hyperscaler’ cloud providers (like Amazon, Microsoft, Google, Alibaba) are both IKEA and Airbus/ASML hard to replicate. They offer a huge and complete range services that are also incredibly advanced and years ahead of commodity products

- Europe has precisely nothing that competes, and is 100% dependent on the ‘IKEA clouds’. We only have partial companies.

- Fixing that situation will not be possible through legislation, standardisation or concerted government action. You can’t procure a competitive mega cloud into existence. Europe did assemble Airbus from its component parts but it was very hard

- Although IKEA exists, you can still get (better) furniture from more specialised places. A European owned email, communication and collaboration cloud might be a feasible idea

- European procurement law makes it entirely doable for governments to order their services from such European communication clouds

- From that, a more viable European cloud ecosystem could perhaps evolve

The longer story:

Computer systems, within governments, in industry and at home, are moving to the cloud at a rapid clip. Some fields have moved almost entirely already - try buying a security camera that is not tied into the cloud, for example. And there’s almost no large company left that still does their own email. Governments are hanging on though.

The landscape can be confusing however - what is “the cloud” even? In a very real definition, the cloud is nothing but “other people’s computers”. However, there is more to it than computers. Lots of things companies and governments used to do themselves is now being delivered “as a service”. This is not a new trend - it was a long time ago when you had to generate your own electricity, for example. We get our electricity from utilities, from a power cloud if you will.

It is only exceptional places that can generate their own electrical power if need be (data centers and hospitals for example). And this is an apt analogy of where computing is heading. Almost everything is supplied and operated by a third party, with rare exceptions. But even these exceptions (elections, military, courts, intelligence agencies, core government departments etc) are struggling to retain their “on-premise” computer programs.

In this piece I want to sketch the cloud situation a bit, and specifically Europe’s lamentable position. As I quoted an EU official earlier, “Interdependence is natural, even desirable. Over-dependence, however, is not”. And Europe is very much over-dependent on specific technologies from other continents.

One possibility I worry about is that a US based cloud comes under cyber attack, and they have to choose which of their customers they are going to help first. Europe has nothing to fall back on, and might be at the back of the queue. I also worry about the 2024 presidential election and the very long reach of US law.

To sketch the cloud situation here, we’re going to look at three of Europe’s most iconic and successful companies: IKEA, Airbus and ASML.

Credit: Unsplash user Zheka Kapusta, Pixabay user juergenschultze and Guus Hubert

As usual, I want to thank the proofreaders of this article, I could not write these things without you! Furthermore, feedback & reflection is very welcome on bert@hubertnet.nl

The IKEA Clouds

IKEA has no competition, and for good reason. It is nearly impossible to compete with IKEA at what they do. They will sell you almost everything your household needs, including meatballs. And, for most products, they offer a decent range of quality, from really cheap to somewhat expensive. They cover all the bases. IKEA products also tend to be quite good, and probably more environmentally sound than what other places sell.

Now, you could be a smaller furniture vendor and get some business that way, but you’ll always be a niche player. Because you simply can’t match the range and depth of what IKEA offers, let alone at their prices. People go to IKEA because they know they’ll very likely find everything they need there. And probably even more stuff.

If you wanted to compete, you’d have to show up with an almost complete IKEA out of the blue. No one is interested in something that offers similar stuff but only 50% of IKEA’s range. And even if you managed to design a comparable range of products, you’d then spend a whole decade learning how match their price point. In short, there is no competing with IKEA.

In the world of cloud, we have a number of what one could call “IKEA Clouds”: Amazon (AWS), Microsoft (Azure), Google (GCP), perhaps China’s Alibaba Cloud/Aliyun, and maybe Oracle and IBM. These are sometimes also called ‘Hyperscalers’.

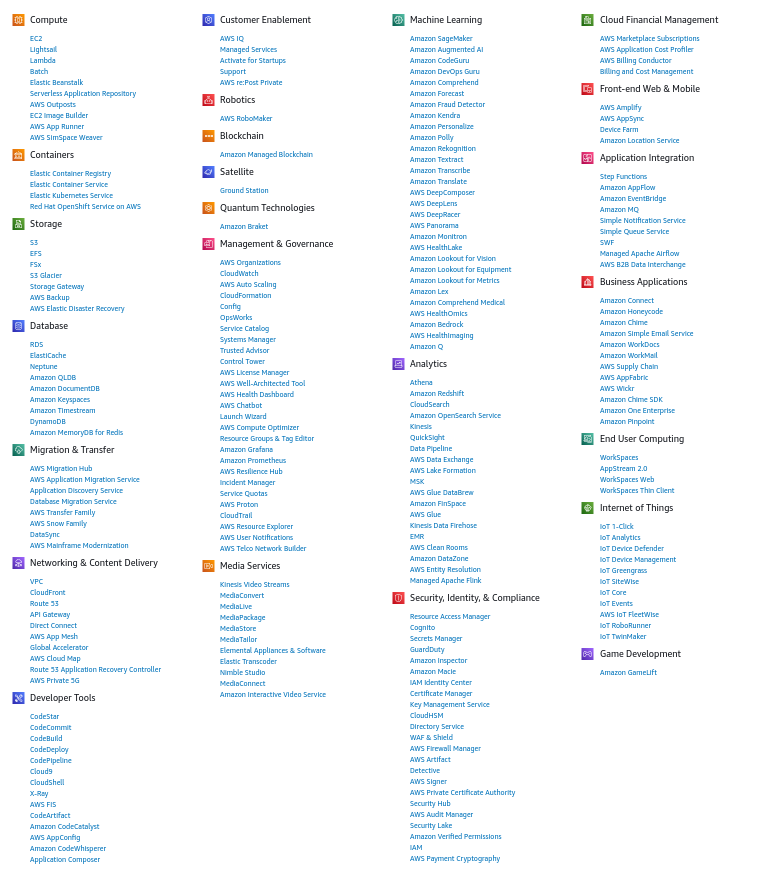

Over at the consoles of these IKEA Clouds, you can find what you need to implement almost every IT solution. Directly and through marketplaces they offer storage, database, email, web shops, AI systems, video streaming, content distribution networks, payment solutions, the works. You can even order a satellite ground station or a private 5G mobile communications backend if that is what you desire (!). Many companies can “just build what they need” using only stock Amazon (market) functionality:

This is a massive catalog. They complete this with certification programs, training, conferences, partners. The whole lot.

To be relevant in this space means showing up with a similar catalog, similar pricing, similar quality levels and a comparable ecosystem. Good luck.

Specifically, for email and office productivity, Microsoft and Google completely dominate that space. This represents an even stronger market dominance than IKEA. For every individual product IKEA sells, you could find something similar elsewhere from another vendor. They just won’t sell you everything you need, but you can get a couch from somewhere else. But if you need corporate email or office productivity, there are only two places to go: Microsoft and Google. However, you could get your other cloud needs from another provider.

Amazon also has an email/calendering offering called WorkMail, but it does not appear to be very popular (but I could be wrong).

Network effects

You can furnish your house with IKEA and non-IKEA furniture without any problem. If you buy an IKEA kitchen however, some network effects appear. You can’t fit many regular ovens in an IKEA kitchen - they use different slot sizes. You have to buy into the IKEA kitchen concept to a certain extent.

Something far stronger applies to the Amazon, Microsoft and Google cloud ecosystems. Their services are all well integrated only within their own cloud. In theory customers could do “multi-cloud operations” but in practice this is very hard to do because these clouds are not interchangeable. Employees that are deeply plugged into one cloud ecosystem really struggle to adjust to another one. Running on three clouds can take twice the headcount, and likely makes your solutions more fragile.

This makes it even clearer that you can only be an “IKEA cloud” if you offer everything customers will ever need. You need to be a one stop shop.

Update, turns out that on the day this post was published, a part of the EU Data Act entered into force, which has components (in chapter VI) that make it (slightly) easier to leave a cloud.

Cloning IKEA

IKEA probably spends tens of millions of euros on designing a new range of office furniture. But not billions. If you’d want to clone IKEA (but why would you want to), you have a lot of work to do. But it is not super innovative work, even though IKEA is very very deep into the experience curve. They are incredibly good at what they do. To get your own IKEA, you will have to work hard and learn a lot. You’ll be losing billions in the first years until you figure out how to also make money at the IKEA price point.

But you don’t need (a lot of) technical breakthroughs.

The cloud is a different story though.

Airbus & ASML

Europe not only has a furniture giant, we also have an aerospace giant: Airbus. There are only two companies in the world where you can buy a modern wide body jet airliner. By understanding the market well and not falling on its face, Airbus is currently very successful. But it took decades to build and assemble Airbus from its many components. But it worked. They also sell satellites, helicopters, fighter jets and military transport planes.

If you want to also get an Airbus (or a Boeing), you’ll not only have to do an “IKEA” in terms of breadth of products, you’ll also have to build and master some very advanced technologies that are not available off the shelf. China has been trying to build a competitive wide body jet for decades, and they still aren’t there. It really is hard. Even Boeing is struggling these days, for example.

A very similar story applies to ASML and its supplier ecosystem. Replicating what these companies have achieved together is proving to be very hard. And in fact, somewhat worryingly, ASML is currently the only place in town where you can get a state of the art wafer stepper, the one you need to make modern and power efficient chips. Geopolitics is playing out, where “the west” is attempting to prevent China from gaining access to these machines (and even to previous generations as well). Despite massive efforts and tons of world class research, China has not been able to setup an ecosystem that can also deliver the infrastructure that can produce the fastest and most power efficient CPUs.

Europe may not have a position in cloud or AI, but all cloud and AI chips are made with ASML devices. Photo credit ASML.

As an aside, a lot could be also achieved by writing more efficient software instead of counting on the fastest chips to speed up the slow code we write these days. One of the founders of modern computer programming (Niklaus Wirth) recently passed away, and he (re)stated it as “software is getting slower more rapidly than hardware is becoming faster”. If we followed his plea for leaner software, data centers could be one tenth of their current size. Perhaps something for Europe to ponder as well?

Scaling the cloud

If we look at the big cloud providers, they offer services at any size you want. Databases and file storage are things you could also source yourself on the open market (for serious money), but every product you buy there has a certain maximum size. If you need a bigger database or need to store more data, eventually you’ll have to re-architect and buy all kinds of new hardware. And, you need to have a large and capable staff that does these things for you.

Not so over at AWS, Microsoft and Google. They offer services that will scale to any size you want. Behind the scenes lots of magic happens to deliver you “infinite” databases and infinite storage that will always work, no matter how much data you put in there, no matter how many rows you put in your database. You will get a truly stunning invoice though, but that’s the only thing you’ll have to worry about.

These and many other services you can buy from the large cloud providers are very impressive and have been honed for years to get to where they are at.

The large clouds also do not run on regular hardware or even regular operating systems. All the major players rely on custom designed chips and/or specialised hypervisors/containers. Also, these cloud players run nation-state level security programs that as far as I know simply don’t exist in European companies.

The Amazon, Google and Microsoft clouds are technological masterpieces, and they are near “Airbus-scale” hard to replicate, if perhaps not quite ASML-level hard.

This does not mean everything is perfect in the cloud. Microsoft Azure has cross-tenant security and stability issues, for example. Amazon’s stuff is getting ever more complex and their pricing can be outrageous, especially when you have no where else to go. And Google has a famously hard time understanding what users need (contrasted with what they think users should need). Finally, many might be frightened of doing business with Alibaba.

The state of the European cloud & Gaia-X

Europe may craft fine furniture and build pretty amazing wafer steppers, airplanes and satellites, but in terms of cloud, the cupboard is almost bare. We do have some small players that deliver parts of the cloud experience. Companies like Scaleway, OVH, Hetzner, Leaseweb, Contabo and ionos. There are also consortia like team.blue and Your.online (formally TWS) that have gobbled up a lot of companies.

But a closer look reveals that most of these only offer the lower end of the stack - (virtual) servers, straightforward hosting, with perhaps some database work. And crucially, none of them offer the “infinite” scaling services for which AWS/Azure/GCP are famous. Nor is there any AI (except a bit over at OVH and Scaleway).

UPDATE: Many people have commented that “Europe simply can’t innovate”, and that this is behind the sad state of affairs. I don’t quite think this is true, but here’s what I wrote earlier on what might be going on with European innovation.

If you know what you are doing, and they sell what you want, these European players can offer pretty good price points, which is one reason why they are still around. But in general, to say that Europe plays a role in cloud is nonsense. We do not have a seat at the table.

Plotting a way back is not straightforward. The rest of the world can also not compete with our IKEA since IKEA already firmly occupies the IKEA position. Righting the ship over at Boeing will also not be easy.

For five years now, there has been a European dream called Gaia-X. Although the aims have shifted, the core idea seems to have been to create uniform standards for common cloud requirements, so that many companies could offer competitive and interoperable services. Gaia-X has not delivered on this, but efforts continue.

You could see some of the logic though - if you want to achieve something grand without actually building a giant “Airbus”, why not set standards so that everyone could build a part. And together, you could assemble this into something big. Gaia-X is/was supported by giant industrial companies and telecommunication firms.

As it stands, it appears unlikely that consensus and standards based efforts governed by lumbering giant companies & the EU can compete with the likes of Amazon/Microsoft/Google. Sorry. Much as I love the EU (what else do we have), they are not in the business of innovating at speed.

Besides Gaia-X, there are now also (semi-)government sponsored initiatives like Catena-x (“Your automotive network”), sphin-x (a health data cloud), manufacturing-x.

As noted above, Europe is now 100% dependent on clouds (and incidentally, hardware) from whole continents away, and this is probably not smart in the long term.

Despite the probable good intentions of Gaia-X, sphin-x, Catena-X etc, it appears unwise to attempt to create a European hyperscaler cloud player only through standards & our lumbering industry. There are also initiatives to use regulatory pressure to force the use of European cloud providers. This makes as much sense as forcing radio stations and Netflix to play more European content (which we are actually appear to be doing).

Some people might also favor doing the big government thing and attempt to create a European cloud by procuring one, or attempting to assemble a ‘cloud Airbus’. I’m not sure if anything like that has ever worked though. Creating Airbus was hard enough. ASML’s creation story also involved government action.

It should be noted however that governments themselves are large scale buyers of software and cloud technologies, and this is where they could do a lot of good.

Things that could be done

There are some other things where governments could help enormously though.

For email, we are heading to a crunch point. Almost all of industry has moved their email to Google or Microsoft cloud services. But European governments can’t yet do this (mostly). Meanwhile, Microsoft has once already stated that you eventually will no longer be able to run their email software on premise, and that you must move to their cloud. They walked that back for now but the writing is on the wall. Soon also no one will have the skills to run their extremely complicated and hard to secure software on-site.

Much like the existence of IKEA does not preclude office or higher-end furniture companies from being successful, it would be entirely possible for someone to create a “government compliant communication services” cloud from Europe. This is not Airbus-level hard. Communication (email, video) is now also intertwined with calendering, scheduling, file exchange, so it is not “just email” you need to sell, and it won’t be that easy to do.

Key there however is that, much like competing with IKEA, this cloud will very much need an edge. A specific reason why people would do business with such a provider, beyond “compliance” or that special EU feeling.

“Digital sovereignty, the strongest argument ever for OVHcloud in the cloud battle”, and comment: “And that is precisely the problem.. we would like the technology to be its best argument.”

As a case in point, the German government appears to have been creating such a government-ready platform, but then decided to give 3 billion euros to Oracle (of all places) instead.

As Amazon founder Jeff Bezos once supposedly said, “your margin is my opportunity”. It turns out that the big cloud providers are currently not that cheap. In fact, they often are surprisingly expensive. This does not mean that most people could save money by buying and operating their own hardware, but it does mean that places that pay attention to what they do can significantly undercut AWS/Google/Microsoft pricing.

This in turn means that a European communication cloud could be competitive on price.

Governments could be key to making this happen. Unlike companies, governments can and should think about more than getting “the best stuff for the lowest price”. Although procurement law does appear to force governments to do this too, it turns out European procurement law most certainly makes it possible to introduce specific requirements and criteria that allow non-incumbents to have a fair chance.

For example, as part of a tender, a government could very reasonably require that the chosen vendor can not be forced by any non-EU government to provide access to your data. This automatically rules out everyone hosting on Google, Microsoft or Amazon or any Chinese owned cloud.

It would be great if we had outfits that offered and sold government compatible services that compare favorably with the communication offerings of Microsoft and Google, which are not widely loved but are deeply entrenched. Once established, such government compatible services might in turn be very attractive for (larger) European companies as well.

And who knows, this might grow into a real European cloud player.

Summarising

Europe currently has no credible cloud position. Having a cloud is not just a matter of buying a lot of hardware, the modern “IKEA clouds” come with a huge array of services, and this alone makes it hard to compete with them. Why do business with a younger less established Amazon that also does not offer everything you need?

In addition, the modern cloud providers are technically very advanced, so substantial work is required to catch up to even where these providers are today. And by the time you do, you are where they were in 2024.

The experience of Airbus and ASML shows that Europe most definitely can do difficult technical things, but also that it takes a long time to get there. The cloud moves faster than that.

The existing clouds however are not that cheap, and specific high need/high requirement communication services could most definitely be cloned in Europe. Governments could be the first buyers since they are driven by more than price alone. Procurement law also makes it possible for such new efforts to succeed.

And once such a government-ready communication cloud is established, it could perhaps grow into an actual European cloud industry.